Understanding Your Administrative Fume Date

Executive Summary

- A wind-down isn’t what happens after strategy fails – it is the final play of the game

- A lot of end-of-business trouble is avoidable with a solid playbook written early and informed by sober and up-to-date financials and realistic timelines

- An uncontrolled wind-down invites fiduciary risk — and exposes the board and officers to financial, legal, and reputational fallout

- A carefully constructed wind-down plan allows a company to responsibly put their last drops of cash toward a rescue plan — and can buy precious days to put a rescue plan in place

- Knowing the administrative fume date — the last day when an orderly wind-down is still possible — helps prevent crash landings that expose directors to unnecessary risk

The Cost of a Crash Landing

“How many days of cash do you have left?” I recently asked a startup board member who had reached out for help.

“About a week,” he replied.

He knew that wasn’t good. But what made his situation truly perilous was his inability to answer my immediate follow-up: “How much is it going to cost to wind down the company?”

Anyone who has served on a startup board has seen “hope springs eternal” up close. It is easy to understand the psychological impulse to keep pushing, even when heading straight for a financial cliff.

However, directors of companies at risk of dissolution expose themselves to severe personal risk by making an easily avoidable mistake: not knowing their administrative fume date.

This structural blind spot is common in early-stage ventures. Without deliberate planning—and without budgeting explicit time and money for a controlled wind-down—start-ups routinely find themselves tens of thousands of dollars short of what is required to exit cleanly.

By that point, many partners and employees associated with the venture are already focusing on their next opportunity. Crashing through a wind-down with insufficient resources and compressed timelines presents acute regulatory, fiduciary, financial, and reputational risks to directors and officers personally.

A Strategic Effort, Not a Post-Strategy Errand

No one is happy when a company shuts down. But the precise way it shuts down matters immensely to employees, fellow directors, investors, future collaborators, and your own long-term professional standing.

The wind-down process should be handled as a professional, deliberate, and well-regarded corporate campaign. If it is sloppy, rushed, or opaque, it rapidly erodes market trust—while inviting immediate confusion, operational conflict, and severe reputational blowback.

Furthermore, unplanned but mandatory emergency administrative work always becomes exponentially more expensive. This introduces unexpected cost overruns that are sometimes born by the directors and officers personally.

Board and management teams should never wait until the walls are closing in to address this reality. Well before cash reserves run thin, leadership should actively ask: In the event of an emergency, what would it take to shut this enterprise down properly?

Just like standard corporate succession or key-person planning, a wind-down playbook does not need to be overly complex at first, but it must exist.

Crucially, it must be formally revisited after major corporate events—especially following new fundraising rounds or taking on a significant new creditor. These milestones fundamentally alter the liquidation waterfall, shift governance rights, and dramatically escalate the dollar amounts involved.

Runway Math and How Not to Be Caught Off Guard

In my experience, companies most often miscalculate their true cash runway in two distinct ways.

1. Over-simplified math leads to over-simplified planning

The most instinctive formula leadership uses is a basic linear calculation:

Cash ÷ Burn Rate = Time Remaining

While instinctive, this formula is dangerously incomplete. It provides a convenient excuse for sloppy thinking around the corporate endgame because it completely ignores existing liabilities and the non-trivial costs of winding down a business responsibly.

A more realistic, structurally sound formula for board-level planning is:

(Cash + Liquid Assets – Liabilities – Wind-Down Expenses) ÷ Unavoidable Burn = Time Remaining

This version forces a much more honest view of capital allocation. It deliberately strips out “soft” assets—like projected R&D tax credits or overvalued inventory—and factors unavoidable shutdown liabilities directly into the calculation. It also clearly outlines which operational levers can still be pulled if no more venture capital can be raised.

2. Misunderstanding how accrual accounting distorts reality

Board members, especially those newer to GAAP principles, are routinely caught off guard by how accrual-basis accounting can obscure a company’s true operational standing. The standard balance sheet may reflect assets or liabilities months before or after the cash actually moves.

Large entries on the balance sheet—such as front-end R&D expenditures capitalized as intangible assets—can severely confuse an assessment of what a company is actually worth and what assets could realistically be liquidated to pay immediate bills.

This disconnect between accounting reality and cash reality leads to false confidence, or conversely, unnecessarily low confidence that paralyzes timely decision-making.

To prevent this distortion once cash on hand starts to tighten, leadership must enforce two adjustments:

- Frequent cash-basis reporting: The CFO or lead accountant must deliver frequent, cash-based updates that are explicitly designed for the board and management team to interpret quickly.

- Legal counsel integration: Near the end of a company’s lifecycle, legal counsel should be actively involved to flag off-balance-sheet obligations and exit penalties embedded in active contracts.

If secured debt is on the balance sheet—particularly if it involves personal guarantees or intellectual property as collateral—it is critical to understand the precise covenants, triggers, and rights of the lender. In these scenarios, wind-down planning becomes materially more complex and must be handled as a tightly coordinated legal and financial exercise.

Whenever financials are updated, one core question must rise to the top: How well do we understand the full cost of winding down—and at what exact point will we no longer be able to afford it?

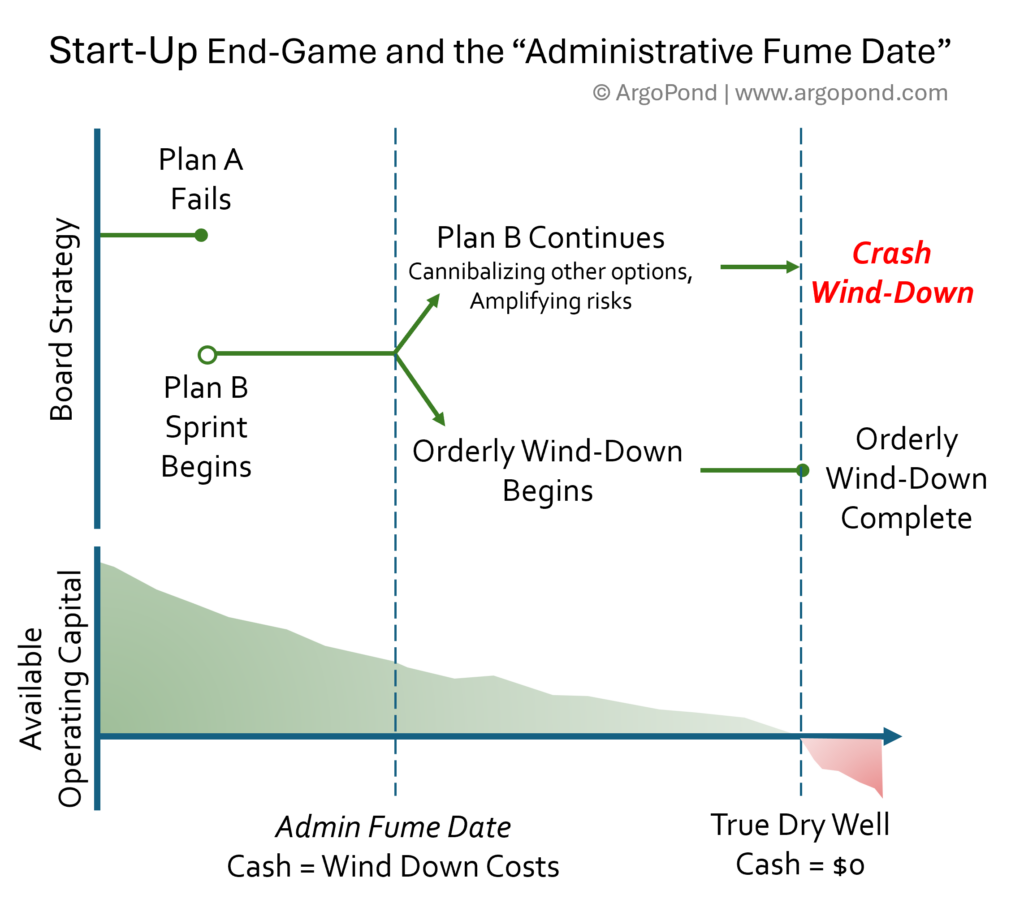

That precise intersection is the administrative fume date: the absolute last calendar day a professional, orderly wind-down is still possible. After that date passes, there will simply not be enough cash left to cover existing obligations and new shutdown costs.

Understanding Your Administrative Fume Date

In bankruptcy law, the “zone of insolvency” refers to the period when a company faces a growing risk of being unable to meet its obligations. While the broader legal implications—including a shift in fiduciary duties beyond equity owners toward company creditors—are beyond the scope of this article, the concept itself is vital for operational planning.

It is within this zone that the tactical concept of the administrative fume date becomes critical.

This threshold marks the point at which a company’s remaining cash reserves exactly equal the calculated cost of a controlled shutdown. Beyond this line, even basic administrative steps—final payroll, vendor notifications, state dissolution filings, legal fees, and accounting costs—become entirely unaffordable.

Directors who allow a company to drift past this threshold without a structured plan risk long-term personal, legal, and reputational fallout. Just as concerning, there may no longer be funds available to bring in outside advisory help to manage the crisis.

As the trajectory graph demonstrates, a company typically flags the severity of its position the moment Plan A—usually a primary financing event like a priced venture round or a critical convertible note—fails to materialize. At this exact inflection point, directors and officers understandably pivot to a Plan B. This is almost always a resource-intensive sprint toward a narrower operational rescue option: an accelerated strategic acquisition discussion, a major grant decision, or a single enterprise customer contract.

Pursuing a Plan B rescue track is not inherently the mistake. The systemic governance failure occurs because this emergency sprint is rarely budgeted in parallel with an explicit wind-down track. As the venture’s cash position drops down the slope, it quietly crosses the administrative fume date line.

If the board takes no structured action at that exact threshold, the Plan B sprint continues entirely at the expense of the company’s structural capacity to shut down responsibly. Remaining capital is completely cannibalized, mandatory obligations are missed, and the terminal outcome is a non-compliant crash wind-down—a messy, chaotic closure that dramatically maximizes personal liability and long-term reputational exposure for directors and officers alike.

Critically, calculating a fume date does not have to mark the end of forward motion. If a wind-down budget is created well in advance, leadership still has the operational runway to pursue investment, sell off core assets, or negotiate strategic exits—but only within a highly disciplined structure. Without that structure, Plan B ceases to be a strategy and instead becomes a corporate delusion, cannibalizing the company’s final resources and amplifying personal risk for everyone involved.

Key Elements of Wind-Down Planning

Wind-down planning does not have to be overly elaborate, but it must be honest, specific, and initiated early. A basic reserve estimate, broken down into clearly defined operational buckets, dramatically improves execution while insulating the board.

A responsible wind-down reserve must account for liabilities across four main categories:

1. Operational Wind-Down Liabilities

- Customer refunds: Accounting for unfulfilled or partially delivered products or subscription services.

- Vendor expenses: Clearing outstanding accounts payable, work-in-progress, and unbilled pass-through expenses.

- Lease liabilities: Managing unpaid rent, mandatory restoration of facilities to “broom clean” conditions, and the potential reversal of tenant modifications.

- Inventory liquidation: Handling unsold inventory, physical material disposal costs, and warehouse clean-out logistics.

- Intangible asset monetization: Offsetting broker and investment banker fees for IP or proprietary data sales, ongoing asset maintenance, and specialized legal reviews of transfer rights and consents.

2. Employee and Compliance Obligations

- Final payroll clearing: Ensuring final paychecks and critical employer-side taxes (FICA, Medicare, and state withholding) are completely funded.

- Benefits and severance: Payout of accrued paid time off (PTO) and any contractually mandated severance obligations.

- Retirement contributions: Transmitting outstanding 401(k) contributions, including withheld employee deferrals that have not yet been sent to the provider.

3. Governance and Risk Mitigation Costs

- Insurance tails: Securing tail policies for all primary corporate coverage, including Directors & Officers (D&O), employment practices, and general and product liability.

- Professional advisory reserves: Funding legal, accounting, and specialized advisory fees. (Note: During a wind-down, you should encourage providers to switch to a single, paid-upfront flat fee to prevent late-arriving service invoices from hitting after bank accounts are entirely frozen).

- Data archiving: Ensuring long-term document retention and secure archival access to corporate email, historical financials, and digital records.

4. Final Communications and Closure Logistics

- Investor relations: Managing mandatory investor elections, cap table notifications, and formal dissolution approvals.

- Vendor and public notifications: Supplying formal notice to active vendors and executing public notices of dissolution, which several states legally require or strongly recommend in advance of a wind-down.

Time-Dependent Wind-Down Triggers

In addition to budgeting raw capital, effective wind-down planning must account for minimum time intervals required by law, contract, or regulatory bodies. These time-triggered milestones cannot be compressed once the clock begins ticking—and rushing them introduces severe compliance exposure.

A critical point regarding timelines is this: someone inside the company must continue to draw a paycheck until these final structural items are executed. That ongoing administrative salary expense must be calculated and included within your wind-down planning.

Consider these common timing requirements when constructing the terminal roadmap:

- Investor/Shareholder Notifications: Many corporate bylaws or investor rights agreements require a strict 10–30 days’ advance notice before holding an extraordinary meeting or taking formal corporate action, such as approving an asset sale or electing a liquidator.

- Board Consents: Even unanimous written consents can take several days to circulate, review, and finalize, particularly when dealing with busy or checked-out directors.

- The WARN Act: Employers approaching certain headcount thresholds may be legally required to provide a 60-day advance notice before executing mass layoffs or facility closures under federal or state WARN Acts.

- Final Paycheck Regulations: State labor laws are rigid. Depending on the jurisdiction, final pay may be required on the exact last day worked or within a strict 72-hour window.

- 401(k) Plan Termination: The IRS and third-party administrator timelines required to officially terminate a retirement plan, issue participant notices, and execute final fund distributions typically span 30–90 days.

- Customer Contract Terminations: Commercial enterprise or health payor agreements frequently require advance written notice (often 30 to 90 days) to legally terminate services without triggering breach clauses.

- Subscription and Software Cancellations: Corporate SaaS stacks and critical software licenses almost always auto-renew annually unless formal cancellation is submitted during an explicit window, often 30 days prior to renewal.

- State Corporate Dissolution: Obtaining formal tax clearance certificates or processing final state filings frequently takes weeks or months to prepare and clear state registries.

- Final Tax Filings and Capital Returns: If residual cash is successfully distributed to shareholders, the company must still file final tax returns and issue corporate 1099s or K-1s during the following calendar year, which is governed by IRS timelines, not the company’s internal schedule.

Conclusion: Leading Well Through the Full Lifecycle

The reality of early-stage innovation is stark: most venture-backed companies do not survive. That is not a pessimistic outlook; it is a clear statistical baseline.

What separates elite, high-integrity corporate leadership is not just how execution is handled during phases of aggressive upward growth, but how operations are managed when that growth stops.

A corporate wind-down is not an inherent failure—it is a distinct operational phase. If managed with precision and foresight, it completely protects core employees, preserves institutional relationships, insulates personal liability, and reflects exceptionally well on the professional reputations of everyone involved.

Planning for the end does not invite failure; it actively prevents chaos.

Inquiries regarding corporate wind-down planning, operational stress-testing, or board governance assessments may be directed to jyounger@argopond.com.

Disclaimer

This white paper is published by ArgoPond, LLC for informational and educational purposes only. It does not constitute formal legal, financial, accounting, or tax advice. The content reflects general principles of corporate governance, budgeting, and fiduciary responsibility relevant to early-stage, venture-backed medtech companies, but it is not a substitute for professional guidance tailored to specific circumstances. Situations involving insolvency, wind-downs, or fiduciary exposure are highly fact-dependent and should always be evaluated in direct consultation with qualified legal, financial, and advisory professionals. No attorney-client, advisory, or fiduciary relationship is created by the use of this document.